Trying to keep up with the explosion of tech buzzwords (and their alphabet soup of acronyms) is becoming increasingly difficult. Every day, we hear about a new tech set to “disrupt” the supply chain space in profound and spectacular ways — IoT, machine learning, neural networks, 3d printing, robotics, AI, VR… the list goes on. Finding ways to leverage this tsunami of technology can quickly become overwhelming — if not impossible.

So, when we bring up blockchain, it can be easy to get dismissive. It’s complicated, somewhat new, and certainly in the group of “disruptive” technology that’s thrown around as the savior of the modern supply chain. But there’s tangible value trapped inside of blockchain, and not only does it have the genuine potential to reduce frictions in the increasingly complicated supply chain, but it’s already being championed by major brands like IBM.

Let’s demystify blockchain and talk about how it will (and is) impacting supply chain management.

Understanding Blockchain (A Guide for Supply Chain Management)

Blockchain technology offers a decentralized database of transactions that are recorded onto blocks of data (hence “block”) and encrypted with cryptography hashes that lead back to the last block created (hence “chain”). At its core, blockchain is a public record of transactions. But, instead of a middleman controlling the distribution and verification (a.k.a “the ledger”) of those transactions, thousands of computers connected to a network agree on valid transactions together.

That may sound a little complicated. So, let’s look at a very common example — currency. Blockchain technology works with any transaction that has value (e.g., currency, property, goods, contracts, etc.) In the typical banking model, the bank verifies the funds in your account. It’s the single source that tells you how much money you’ve spent and how much money you have left in your account. How do you really know that you only have $3,117 in your checking account? The bank tells you that you do. You have to trust what they say.

With blockchain, every transaction is recorded onto a digital block, secured with a cryptographic hash of the previous transaction (every new transaction links back to all of the previous ones), imprinted with a timestamp, and verified by all other computers connected to the network. The bank doesn’t act as a single entity that decides transaction value — the community does. It’s decentralized.

This decentralization is the fuel that makes blockchain such an explosive tech revolution. The most famous example of blockchain is Bitcoin. Satoshi Nakamoto outlined the idea for blockchain in a whitepaper detailing his creation of a new digital currency (i.e. Bitcoin). This new currency would be decentralized, and, instead of relying on a bank to produce and maintain a ledger of transactions, Bitcoin would rely on thousands (now millions) of computers connected to a network.

Every new Bitcoin transaction is encrypted and verified by all computers on a network. And, once verified, it’s added to the chain of other transactions, timestamped, and cryptographically secured — at which point it waits for another transaction to add onto the chain. Every new transaction is a new block, and all of the computers work together to create the computing power required to encrypt each block.

Blockchain technology has four core attributes:

Decentralization: Data is shared by everyone — not owned by a single entity.

Immutable: Data can’t be tampered with. Not only does blockchain requires sharing blocks with everyone in the community (threat actors would need to access everyone’s computer instead of a single, core entities data), but every block is cryptographically secured using significant computing power that’s generated via all of the computers connected to the network. In other words, a threat actor would need to both access everyone’s computer and change everyone’s digital ledger, and generate more computing power than every other computer on the network.

Transparency: Every new transaction that takes place is visible. So, if a manufacturer creates a new transaction, their identity (at least their network identity) will show that they have created that transaction. Let’s make a clarification. Blockchain doesn’t have to be 100% transparent. You can still encrypt supply contracts and use permission-based sharing to keep sensitive information private. But it emphasizes sharing as a mode of necessity.

Costless: The blockchain model is automated. You don’t have to pay a source for each new transaction that’s generated.

The Value of Blockchain for Supply Chain Management

Blockchain has the power to automate components of the supply chain, breed high levels of transparency between suppliers and manufacturers, reduce waste, reduce prices and bottle-necks, and increase collaboration all within a shared economy. Let’s take a look at some of the ways that blockchain can disrupt supply chain management across industries.

Breeding Transparency

Supply chain management is incredibly complex. A single product can have a supply chain that varies in geography, involves hundreds (if not thousands) of entities, and generates hundreds of unique transactions. During this entire complex process, transparency is virtually non-existent. The globalization of the world’s supply chain involves too many moving parts and foreign manufacturing and sourcing to effectively track and manage in its current state. This leads to a plethora of problems.

For starters, consumers and businesses have a difficult time assessing the value of goods. Where did they really come from? Who really made them? There’s also the issue of fraud. If any player in the supply chain is committing fraud or other illicit activities, tracking that fraud throughout the ever-expanding web of suppliers and buyers is nearly impossible. The supply chain contains information silos on virtually every layer.

Our modern supply chain is hinged on trust. If you can’t trust everyone in the chain and their data and information, you can’t accurately forecast trends, demands, and supply. But how do you know if you can trust everyone?

Blockchain is data silo kryptonite. Since every transaction that takes place on the blockchain is attached to an entity, every move on the chain is immediately visible to everyone else. This breeds honesty, trust, and responsibility throughout the supply chain without interrupting the flow of materials with burdensome manual touchpoints. In other words, blockchain doesn’t rely on stakeholders in the supply chain to trust each other. Trust is built directly into the system.

Policy

Detecting and mitigating fraud and illicit activity in the supply chain is impossible. You don’t control the platform. When suppliers hand over data or share information, you have to take that information and apply it to your operations. There’s no checkpoint. So, if there’s one weak link anywhere in the supply chain, those burdens fall onto your lap. The supply chain is only as strong as its weakest link.

Blockchain has no weak links. Every transaction is recorded and verified by everyone. All activity is easily traceable, and every transaction is immediately accessible for all parties. If there’s illicit or fraudulent activity, it’s visible to everyone — from suppliers to producers to customers. This makes the governance of policy systematic instead of granular.

Of course, not everything can be visible, and blockchain solutions targeting supply chain management will certainly need to have blended environments. For example, contracts can’t be visible to everyone, and there is certainly data that simply can’t be shared. So, when we talk about blockchain in relation to the supply chain, the solution will need to be novel (see IBM’s solution at the end of this post.)

Blockchain can’t be copy-pasted into supply chain management. Solutions will need to be built from the ground up for the sole purpose of supply chain management, and the end solution won’t resemble more popular blockchain tech (like Bitcoin) in many ways.

Decentralizing the Supply Chain Economy

Every supply chain has bias. When each stakeholder in the chain has access to their own data, sharing that data is dependent. How do you know that your supplier is really giving you the full picture? How do you know that the supplier before them did? This trickles down the chain. Since you can only rely on the supplier before you, the supply chain suddenly becomes centralized. One authority holds the keys to the data (a.k.a the previous link in the chain).

Blockchain turns this upside down. Suddenly, everyone holds the keys to data. And, given that the data is immutable, values are true-to-life all the way down the chain. Not only does this breed responsible actions and give you the ability to instantly trace any code of conduct violations, but it removes data as an instrument of bias. Everyone gets the data, and you don’t have to rely on the goodwill and good intentions of every other link in the chain.

Reducing Costs for Everyone in the Supply Chain

All of us are on a quest for efficiency and cost-reduction. Between lean manufacturing models — like Toyota’s LEAN — and outsourcing, finding ways to cut costs and boost productivity are key concerns for everyone in the supply chain. Globalization has tightened margins and finding ways to win as a supplier or producer requires a heavy focus on cost-cutting.

Blockchain sews together the gaps in the supply chain. Instead of relying on risky 3rd party data, you get a clear view of the entire chain. This gives you the ability to identify weak points and create systematic changes to enforce your lean agenda. Full transparency can lead to rapid cost reduction.

To really understand the full scope of blockchain when applied to the supply chain, let’s take a look at a real-life example of blockchain in action. Namely, let’s look at how IBM’s Food Trust blockchain network is reshaping the food supply chain.

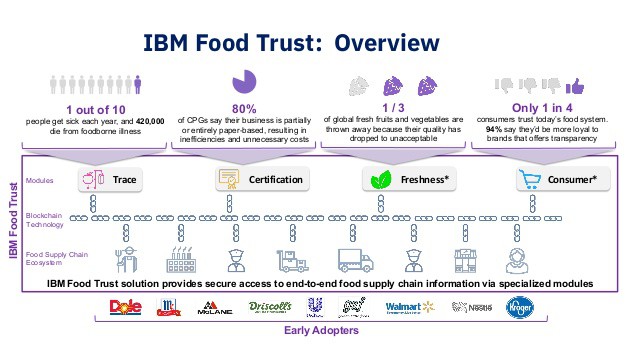

An Example: IBM Food Trust

One of the biggest problems facing the global food supply chain is transparency. Consumers are increasingly health-conscious, and 48% of consumers are willing to completely change their purchasing habits to support sustainability. IBM has built Food Trust — a blockchain solution aimed at promoting transparency in the food supply chain.

Users can instantly access critical information regarding food items in real-time by leveraging the Global Trade Item Number (GTIN) or Universal Product Code (UPC) of the item. Users can view safety information, sourcing, location, and credibility of any products in their supply chain (both upstream and downstream) in an instant. IBM built out a solution that automates the data ingestion layer for businesses, but still gives them permission-based sharing (i.e., they can choose what to share). This blended transparency model (i.e., “transparency with permission”) provides businesses with the flexibility to retain business-critical information, but it also provides every layer of the supply chain with an urgency to share data. If a supplier is not willing to share data regarding a credibility check on their products, producers can quickly choose a supplier who will.

For the food industry, freshness, risk containment, and quality are all key values. Food Trust lets anyone see dwell time, time-since-harvest information (product age), and the overall volume at each processing facility. Of course, this includes the ability to detect risk rapidly. If an outbreak happens at a facility, anyone can quickly see if any of their food came from that facility or specific farms. That means faster contamination containment and reduced risk both upstream and downstream.

There are some extra functions baked into IBM’s tech. You can create smart contracts leveraging the immutability of blockchain to automate decision making. Of course, these contracts take place in encrypted channels where data is only shared between the two primary parties — not the entire blockchain network. IBM also leverages an Advisory Council to ensure governance of data across the blockchain ledger.

Here’s where things get interesting. IBM doesn’t have unique access to any of the data generated in this blockchain. Remember, blockchain is decentralized. IBM isn’t a single entity that stuffs data in the cloud. Everyone can see all of the data shared in the network. And, of course, some data can be held private for business reasons, and contracts between parties are encrypted on separate encrypted blocks.

Want to learn more about IBM Food Trust? Click here.

What Does This Mean for Consumer Product Goods Companies?

The future of your supply chain may be blockchain. Of course, reliable, hyper-functional blockchain infrastructure that can tackle consumer goods is still on the horizon. While IBM pioneers blockchain for the food ecosystem and new brands secure funding for blockchain infrastructure daily, preparing yourself for the new age of supply chain transactions requires forward-thinking and a willingness to adopt data-first principles.

Lanyap Financial is a tech-based accounting and financial services firm that specializes in streamlining their clients’ financial operations through FinTech software and cloud-based applications.